All Categories

Featured

Two individuals purchase joint annuities, which offer a guaranteed revenue stream for the remainder of their lives. When an annuitant dies, the interest gained on the annuity is dealt with in different ways depending on the type of annuity. A kind of annuity that quits all repayments upon the annuitant's fatality is a life-only annuity.

If an annuity's designated beneficiary dies, the outcome depends on the certain terms of the annuity contract. If no such recipients are assigned or if they, also

have passed have actually, the annuity's benefits typically advantages usually change annuity owner's proprietor. If a recipient is not named for annuity advantages, the annuity continues commonly go to the annuitant's estate. Annuity death benefits.

Is an inherited Annuity Payouts taxable

This can give greater control over exactly how the annuity advantages are dispersed and can be component of an estate planning method to manage and protect properties. Shawn Plummer, CRPC Retirement Coordinator and Insurance Representative Shawn Plummer is an accredited Retired life Coordinator (CRPC), insurance representative, and annuity broker with over 15 years of direct experience in annuities and insurance coverage. Shawn is the creator of The Annuity Specialist, an independent on the internet insurance coverage

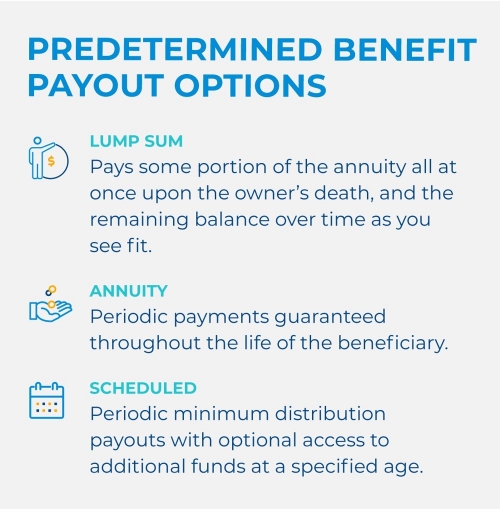

firm servicing consumers across the USA. Via this system, he and his team purpose to eliminate the uncertainty in retirement preparation by aiding people find the most effective insurance protection at one of the most affordable prices. Scroll to Top. I understand all of that. What I don't comprehend is just how before entering the 1099-R I was revealing a refund. After entering it, I now owe taxes. It's a$10,070 difference between the reimbursement I was expecting and the tax obligations I now owe. That seems extremely severe. At most, I would certainly have anticipated the refund to reduce- not completely vanish. An economic consultant can help you determine exactly how ideal to handle an acquired annuity. What occurs to an annuity after the annuity owner passes away depends on the regards to the annuity agreement. Some annuities simply quit distributing income settlements when the proprietor passes away. In lots of cases, nevertheless, the annuity has a survivor benefit. The beneficiary might receive all the remaining money in the annuity or a guaranteed minimum payout, usually whichever is greater. If your parent had an annuity, their agreement will specify that the recipient is and may

into a pension. An acquired individual retirement account is an unique pension made use of to disperse the possessions of a deceased individual to their recipients. The account is registered in the departed person's name, and as a beneficiary, you are not able to make added contributions or roll the acquired individual retirement account over to an additional account. Just qualified annuities can be rolledover into an acquired IRA.

{kind=link}

Latest Posts

Highlighting the Key Features of Long-Term Investments Key Insights on Fixed Index Annuity Vs Variable Annuities What Is the Best Retirement Option? Advantages and Disadvantages of Different Retiremen

Exploring What Is Variable Annuity Vs Fixed Annuity A Comprehensive Guide to Investment Choices Breaking Down the Basics of Investment Plans Features of Smart Investment Choices Why Fixed Vs Variable

Understanding Variable Annuity Vs Fixed Annuity Key Insights on Annuity Fixed Vs Variable Breaking Down the Basics of What Is A Variable Annuity Vs A Fixed Annuity Features of Fixed Index Annuity Vs V

More

Latest Posts